- B-R & H Finance - The 4 Seasons

- Posts

- B-R & H Finance ● The 4 Seasons

B-R & H Finance ● The 4 Seasons

Mid-April 2026

William Bowdler-Raynar

April 15, 2026

Gemini - Homage to Dali

Table of Contents

B-R & H Finance - Purely indicative - 15.04.2026 / 12h CET

B-R & H Finance - Purely indicative - 15.04.2026 / 12h CET

B-R & H Finance - Purely indicative - 15.04.2026 / 12h CET

Market Review

Back to normal ?

Since the start of the month, global equities have moved ahead at a rapid pace, with the main world index up around 6.26%. The leaderboard is dominated by SK Hynix, Micron Technology and Intel, whose monthly gains sit between 20% and 30%, showing that semiconductors remain at the heart of the market’s momentum. At the other end of the spectrum, ServiceNow, Intuit and Atlassian are down roughly 10% to 14% over the period, a sign of rotation within technology itself and renewed pressure on growth‑software names.

In Europe, dispersion is high but the magnitudes are more contained. STMicroelectronics and Nokia are up between 15% and 21% this month, ahead of Vivendi and ArcelorMittal, which are gaining roughly 11% to 15%. In contrast, Hermès International, Accenture and SAP are down around 5% to 7%, while Kering and Kongsberg Gruppa are off about 4% to 5%. The message is clear: European technology is still benefiting from the AI cycle, while luxury and some service sectors are seeing a bout of profit‑taking.

The Swiss market, finally, illustrates how selective investors have become. Inficon, Vat Group and Sika are up between 8% and 16% for the month, with ABB and Georg Fischer adding roughly 6% to 9%. At the bottom of the table, Barry Callebaut, Lindt & Sprüngli, Zurich Insurance and Swisscom are down 2% to 6%, weighed by a tougher backdrop for defensive valuations.

For long‑term investors, month‑to‑date performance is a reminder that index returns conceal very large gaps between winners and losers.

On the commodity side, Brent crude remains under pressure but is no longer rising in a straight line. June 2026 futures trade around Usd 95 per barrel. The market now prices in a persistent geopolitical risk, but is also starting to discount a de‑escalation scenario, while banks such as J.P. Morgan still forecast a much lower average Brent price over 2026 as a whole.

In crypto assets, Bitcoin is trading around Usd 74'000 and Ethereum near Usd 2'370, higher than at the end of March but still below their 2025 peaks. Volatility remains high, fuelled in part by reports that Iran wants to charge some of the transit fees for ships crossing the Strait of Hormuz in cryptocurrencies, mainly Bitcoin, as a way to sidestep the dollar system and Western sanctions.

On interest rates, the yield on the 10‑year US Treasury hovers around 4.3%, slightly above its level at the start of the month but without breaking the existing trend. This relative stability, despite expensive oil and regional tensions, suggests investors still believe in a soft landing for the US economy and in a rate‑cutting cycle that is being pushed back, but not scrapped.

Few numbers

China’s energy dependence remains relatively modest, around 15–25%, thanks to its coal, renewables and nuclear fleet, versus roughly 55–65% for the European Union.

In 2025, China shipped about 5.3 million cars abroad, helped by electric vehicles priced below 10'000 Usd, while the United States exported only around 1.3 million, weighed down by SUV and pick‑up models that are hard to sell overseas.

Seven major hotel chains together owe their customers some 11.6 bn Usd in unused loyalty points, including nearly 4 bn Usd for Marriott and its 271 million Bonvoy members.

Editorial

Armin from X

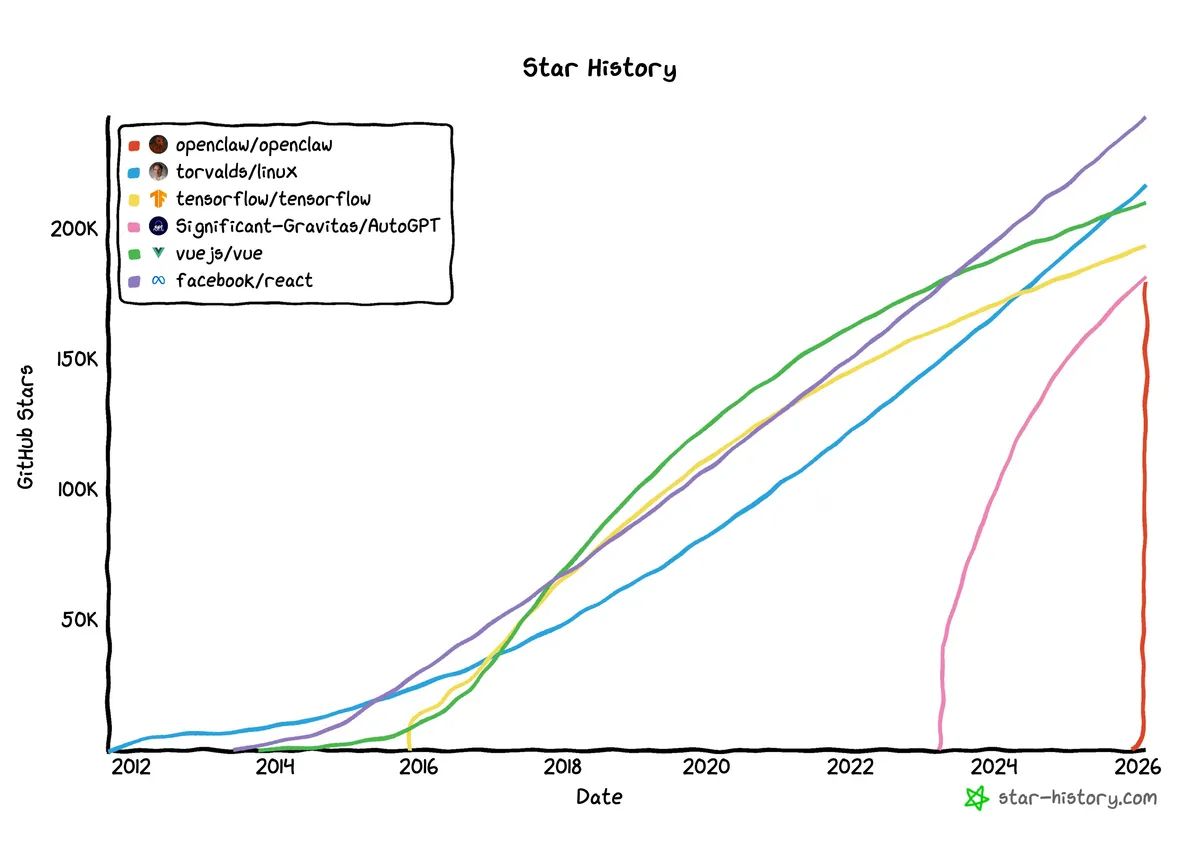

OpenClaw: when one idea is worth a thousand employees

OpenClaw is not just another gadget in the daily AI newsflow; it is a shift in how work gets done. Created by Austrian entrepreneur Peter Steinberger, this digital agent can take control of your computer, open applications, click, code, test, document – like a very disciplined colleague who never tires, never disconnects. Where the previous generation of AI answered questions in a chat window, OpenClaw executes entire projects inside your actual working environment.

After Covid, we learned to distinguish “office work” from “working from home”. That distinction already feels dated. With services like Claude Dispatch, you can send instructions to your desktop from a bus, a massage chair or a beach; in the background, agents like OpenClaw string tasks together, update files, launch simulations. The question is no longer “where do we work?”, but “when do we actually stop working, if our digital twin keeps going without us?”.

This changes the speed at which ideas travel. Peter Steinberger explains that the first version of OpenClaw took him about an hour to build, before the tool was adopted, refined and deployed by hundreds of thousands of users. For those who understand these new tools, the journey between an intuition and a working prototype is now measured in hours, not months: you formulate a goal, let the agent run, then correct at the margins. In the old world, an idea was not enough. You had to hire a team, train, explain, repeat, sometimes for months, before seeing the first usable product appear. Fixed costs, human frictions and staff turnover were part of the background noise.

For established companies, the implication is clear: the challenge is no longer to hire battalions of young graduates, but to find the few people who can think clearly, very fast, and work hand in hand with these tools. Instead of entire departments, you recruit tandems: one profile with vision and deep sector understanding, and one profile able to turn that vision into a product or service within hours, using AI agents. Or, more radically, you look for individuals who combine both dimensions and “multiply” themselves through a digital workforce.

Investors are already talking about the “one‑person unicorn”. Analysts imagine founders capable of building high‑growth companies with a tiny human core, backed by armies of software agents. In 2025, we still talked about “AI‑augmented employees”. That idea is now obsolete: AI is no longer an add‑on, it is the starting point, the foundation of the project, built in from the ground up.

We tend to picture OpenClaw as a way to save time; we forget that, for many, it will mostly create a gap. On one side, a small minority designing products, testing markets, launching businesses almost alone; on the other, a majority still using AI as a slightly improved search engine. Between these two worlds, the gap in skills, wealth and bargaining power could end up resembling the distance that separated 19th‑century industrial entrepreneurs from unskilled factory workers. The question our clients are already asking is simple: which side of that divide do they want their children to live on, and how do they prepare them for it.

Receive market insights (and more) on the first and third Friday of each month.

If you enjoy this newsletter, please share it

Wealth

French property companies: pitfalls to watch

In France, a Société Civile Immobilière (SCI) is in principle tax‑transparent: rents and expenses flow straight through to the shareholders, and are taxed under the personal income tax rules, as long as the company sticks to a “civil” activity (ownership, personal use, unfurnished letting). The picture changes as soon as the SCI starts renting the property furnished, even occasionally via a platform such as Airbnb: this is treated as a commercial activity and pushes the SCI into the corporate tax regime, irreversibly. From that point, the company can depreciate the building, but it must behave like a commercial entity, with more robust bookkeeping, a corporate tax return and no more free accommodation for shareholders, otherwise it may be seen as “abnormal management”. In practice, the manager must either charge shareholders a market rent or set a market‑based notional rent for tax purposes – a surprise for many families who only meant to “cover the running costs” for a few weeks a year.

Even without any letting, a French holiday‑home SCI needs to be run like a small business: a dedicated bank account, clear tracking of cash flows, and decisions recorded in writing, even briefly. The company’s value rests on a well‑defined net asset position (property value minus debt); without basic accounts, the tax authorities are entitled to rebuild that value themselves, often conservatively, with immediate consequences if the numbers are challenged. Cash advances made by shareholders – the “current accounts” that often finance the purchase, renovation or loan repayments – should be framed by a loan agreement and properly documented; if not, they can be reinterpreted as unusual flows with a less favourable tax reading. For any owner, the key questions are straightforward: is the property used purely by the family, or sometimes rented out? If it is, is the letting unfurnished or furnished, and what does that imply for the SCI’s tax status? Are the money flows between the company and its shareholders clear, written down and defensible over time ?

Many problems arise in the grey areas that no one has really put on paper. A house is mainly used by the family, but occasionally lent to friends who “chip in” for costs, or rented out from time to time on a platform, without anyone being quite sure whether this still counts as a civil activity or has already drifted into something commercial. In the same way, some shareholders put in far more cash than others for major works, with no written agreement or clear repayment plan, creating both a tax risk and future resentment. Finally, making the property available to shareholders free of charge is allowed, but it should be backed by a formal SCI decision and remain consistent with the rest of the documentation (by‑laws, minutes, occupancy agreement), so that it can be explained simply if the tax authorities have questions. In practice, taking the time to write down who can use the house, under what conditions, how “mixed” periods (friends, occasional lets) are treated, and how shareholder advances and repayments are handled, goes a long way towards securing the SCI without turning it into a burden.

The best-remembered parties are often the ones you never went to

B-R & H Finance

Founded in 2004, B-R & H Finance SA is a Swiss entity specialized in wealth management. We offer a full range of personalized and independent investment services and advisory solutions. Regulated by SO-Fit and authorized by FINMA, we are also members of the ASG (Swiss Association of Independent Asset Managers) and work with leading custodian banks.

Affiliate Programs and Sponsored Content: Please note that while we strive to provide accurate and up-to-date information, we are not responsible for the content of external sites referenced in our articles, reports, or any other materials. Some links may direct you to affiliate programs or sponsored content, which will be indicated by an asterisk (*). We do not manage or endorse the privacy practices, content, or policies of these third-party sites. We encourage you to carefully read their privacy policies and terms and conditions before engaging with them.

Disclaimer: This newsletter is for informational purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell securities or adopt an investment strategy. The information, opinions, and analyses presented here are based on sources believed to be reliable and are expressed in good faith, but no explicit or implicit guarantee is made regarding their accuracy, completeness, or reliability. Stock market investments are subject to market and other risks, and there is no guarantee that investment objectives will be achieved. Past performance is not indicative of future results.